In a year when Wall Street predicted oil would surpass $100 for the first time in four years, the oil market instead experienced its worst annual loss since 2015.

The oil market's sudden-about face in the fourth quarter has ended a 2½-year recovery for oil prices following the 2014-2016 downturn. Analysts expect oil prices to rebound next year, but the geopolitical risks that have weighed on the market throughout 2018 will remain a big variable in the New Year.

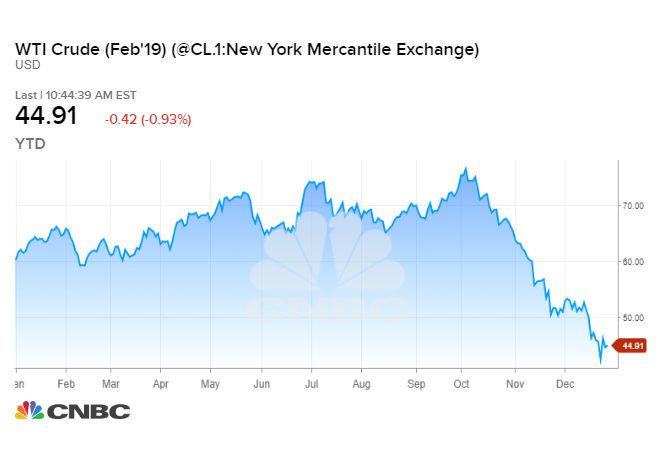

U.S. crude is trading around $45 a barrel, on pace to end the year down 25 percent. At $53 a barrel, international benchmark Brent crude is down about 21 percent in 2018. The declines mark the first annual loss and the biggest yearly drop since 2015, when both contracts fell more than 30 percent.

Just three months ago, oil was trading at nearly four-year highs. While many analysts said the rally was unwarranted and warned a pullback was in the cards, few predicted the market would sell off so sharply. From peak to trough, U.S. crude has shed nearly half its value.

With the benefit of hindsight, it's fairly easy to explain oil's plunge into a bear market.

In May, the Trump administration restored sanctions on Iran, OPEC's third biggest producer, raising concerns about a supply squeeze in the oil market. The following month, OPEC and a group of producers led by Russia abandoned their 2016 agreement to restrict supply. At the urging of Trump and oil customers, Saudi Arabia in particular turned on the taps, adding about 1 million barrels per day to the market between June and November.

But by October, forecasters were warning that demand for oil would grow more slowly than previously anticipated. The same month, the stock market plunged, hammered by a sell-off in high-flying technology equities, the ongoing U.S.-China trade dispute and rising interest rates.

Investors began dumping risk assets, and by the end of the month, oil had plunged about $11 a barrel from its Oct. 3 high. Momentum trading and the rotation out of slumping crude futures and into rising natural gas contracts also deepened losses for oil, analysts say.

Making matters worse, when the sanctions officially snapped back into place on Iran on Nov. 5, President Donald Trump surprised the market by granting generous exemptions to the Islamic Republic's biggest customers. That meant Saudi Arabia, Russia and several other producers had been hiking output into a market where demand growth was moderating and fewer Iranian barrels than expected were lost.

At year end, the U.S.-China trade dispute remains unresolved, and the market remains concerned that a full-blown trade war between the world's two biggest economies will dent fuel demand. Meanwhile, American crude output is growing more quickly than expected, with the United States topping Saudi Arabia and Russia to become the world's biggest producer in the second half of 2018.

However, many U.S. producers need oil prices in the $50-$55 range to break even on the cost of new wells, which is forcing some energy companies to tap the breaks, said Neal Dingmann, oil equity analyst at Suntrust Robinson Humphrey.

"I always say the cure for low prices in the U.S. is low prices," Dingmann told CNBC's "Squawk Box" on Monday. "You're already starting to see a number of U.S. producers starting to back off. We've heard about three or four of the mid-cap companies decide that."

"There's even talk here around Texas in Midland about some of those places starting to at least soften a little bit," he said, referring to the nation's hottest shale oil region.

That could lead to a gradual reduction in U.S. production in the first or second quarter, says Dingmann. That would help OPEC to balance the market in 2019. This month, the 14-nation producer group and its allies reversed course once again and agreed to cut production by 1.2 million bpd.

Wall Street generally sees Brent bubbling back up to roughly $70 a barrel and WTI bouncing above $60. However, there are several key risks that could keep prices volatile, including U.S.-China trade tensions and the expiration of Trump's Iran sanctions waivers around the start of May.

With the political environment still impacting crude futures, it could be more difficult for the oil market to reach equilibrium and investors will have to prepare for more volatility, according to Dingmann.

No comments:

Post a Comment